Cornice

Raumbeispiel

144

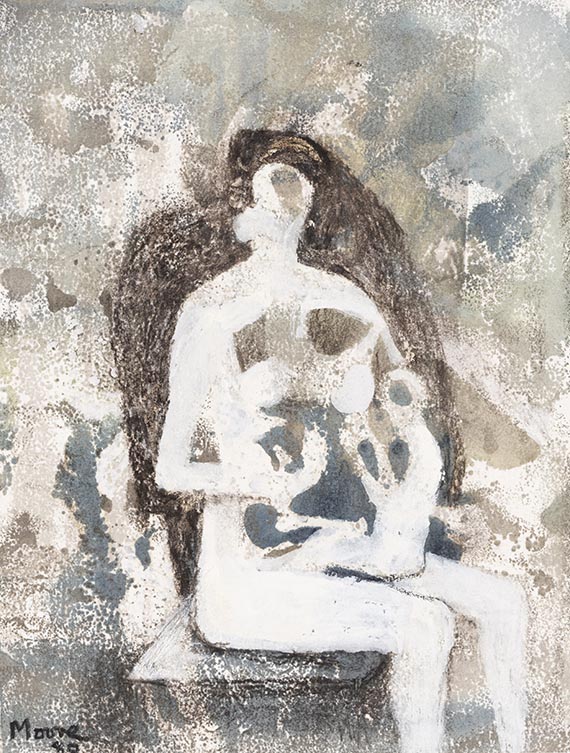

Henry Moore

Seated Mother and Child, 1980.

Gouache and chalks

Stima: € 15,000 / $ 16,050

Seated Mother and Child. 1980.

Gouache and chalks.

Lower left signed and dated. On blotting paper. 22.5 x 17.2 cm (8.8 x 6.7 in), the full sheet. [CH].

Further works from the Dr. Maier-Mohr Collection will be offered in our Evening Sale on Friday, June 7, 2024 and in our Modern Art Day Sale on Saturday, June 8, 2024 – see collection catalog "A Private Collection - Dr. Theo Maier-Mohr".

• The relationship between mother and child is a key theme that Henry Moore worked on almost obsessively.

• From the 1920s until the end of his life, Moore explored this motif in works that range from highly figurative to completely abstract.

• He addressed both the human aspect of the mother and child relationship and the spatial relationship between large and small forms.

• In addition to the sculptural works, the drawings with their sculptural approach to the human form, occupy an extremely important artistic position in his oeuvre.

• This drawing has been in the same German private collection for almost 40 years.

The work is documented at the Henry Moore Foundation, Hertfordshire, with the number HMF 80 (75).

PROVENANCE: Fischer Fine Art Ltd., London.

Dr. Theo Maier-Mohr Collection (acquired from the above in 1985).

Ever since family-owned.

EXHIBITION: Henry Moore. Recent Work, Fischer Fine Art, London, June-July 1980, cat. no. 18 (ilu.).

LITERATURE: Ann Garrould, Henry Moore. Complete Drawings, vol. 5 (1977-1981), London/Much Hadham 1994, no. AG 80.125 (illu. in black and white).

"From very early on I had an obsession with the mother and child theme. It has been a universal theme from the beginning of time and some of the earliest sculptures we've found from the Neolithic Age are of a mother and child. I discovered, when drawing, I could turn every little scribble, blot or smudge into a mother and child. So that I was conditioned, as it were, to see it in everything. I suppose it could be explained as a 'mother complex'."

Henry Moore, in: John Hedgecoe and Henry Moore, Henry Moore, New York 1968, p. 61.

Called up: June 7, 2024 - ca. 14.31 h +/- 20 min.

Gouache and chalks.

Lower left signed and dated. On blotting paper. 22.5 x 17.2 cm (8.8 x 6.7 in), the full sheet. [CH].

Further works from the Dr. Maier-Mohr Collection will be offered in our Evening Sale on Friday, June 7, 2024 and in our Modern Art Day Sale on Saturday, June 8, 2024 – see collection catalog "A Private Collection - Dr. Theo Maier-Mohr".

• The relationship between mother and child is a key theme that Henry Moore worked on almost obsessively.

• From the 1920s until the end of his life, Moore explored this motif in works that range from highly figurative to completely abstract.

• He addressed both the human aspect of the mother and child relationship and the spatial relationship between large and small forms.

• In addition to the sculptural works, the drawings with their sculptural approach to the human form, occupy an extremely important artistic position in his oeuvre.

• This drawing has been in the same German private collection for almost 40 years.

The work is documented at the Henry Moore Foundation, Hertfordshire, with the number HMF 80 (75).

PROVENANCE: Fischer Fine Art Ltd., London.

Dr. Theo Maier-Mohr Collection (acquired from the above in 1985).

Ever since family-owned.

EXHIBITION: Henry Moore. Recent Work, Fischer Fine Art, London, June-July 1980, cat. no. 18 (ilu.).

LITERATURE: Ann Garrould, Henry Moore. Complete Drawings, vol. 5 (1977-1981), London/Much Hadham 1994, no. AG 80.125 (illu. in black and white).

"From very early on I had an obsession with the mother and child theme. It has been a universal theme from the beginning of time and some of the earliest sculptures we've found from the Neolithic Age are of a mother and child. I discovered, when drawing, I could turn every little scribble, blot or smudge into a mother and child. So that I was conditioned, as it were, to see it in everything. I suppose it could be explained as a 'mother complex'."

Henry Moore, in: John Hedgecoe and Henry Moore, Henry Moore, New York 1968, p. 61.

Called up: June 7, 2024 - ca. 14.31 h +/- 20 min.

144

Henry Moore

Seated Mother and Child, 1980.

Gouache and chalks

Stima: € 15,000 / $ 16,050

Commissione, tassa e diritti di seguito

Quest'oggetto viene offerto con regime fiscale normale o con imposizione sul margine di profitto.

Calcolo commissione particolare sul margine del profitto:

- Prezzo d’aggiudicazione fino a 800.000 euro: provvigione del 32%.

- Per la parte del prezzo d’aggiudicazione superiore a 800.000 euro si calcola una provvigione del 27%, che viene aggiunta a quella relativa alla parte del prezzo d’aggiudicazione fino a 800.000 euro.

- Per la parte del prezzo d’aggiudicazione superiore a 4.000.000 euro si calcola una provvigione del 22%, che viene aggiunta a quella relativa alla parte del prezzo d’aggiudicazione fino a 4.000.000 euro.

Il prezzo d’acquisto comprende l’imposta sul valore aggiunto in vigore in quel momento, attualmente il 19%.

Calcolo regime fiscale normale:

Prezzo di aggiudicazione fino a 800.000 €: supplemento del 27%, più l´IVA legale

Prezzo di aggiudicazione superiore a 800.000 €: Parte del prezzo fino a 800.000 € supplemento del 27 %, parte del prezzo che supera i 800.000 € supplemento del 21%, a talvolta maggiorato dell'IVA legale.

Prezzo di aggiudicazione superiore a 4.000.000 €: Parte del prezzo che supera i 4.000.000 € supplemento del 15%, a talvolta maggiorato dell'IVA legale.

La preghiamo di avvisarci prima della fatturazione nel caso in cui desidera applicare il regime fiscale normale.

Calcolo diritti di seguito:

Per le opere originali di arti figurative e fotografie di artisti viventi o deceduti da meno di 70 anni soggette al diritto di seguito, in tutti i casi suddetti viene riscossa in aggiunta, a liquidazione della compensazione del diritto di seguito dovuto dalla casa d'aste ai sensi del § 26 della legge tedesca sul diritto d'autore (Urheberrechtsgesetz, UrhG), una compensazione del diritto di seguito con le percentuali indicate nel § 26 2° comma UrhG, che attualmente sono le seguenti:

4 per cento della parte del ricavo della vendita da 400,00 euro a 50.000 euro,

un altro 3 per cento della parte del ricavo della vendita da 50.000,01 a 200.000 Euro,

un altro 1 per cento della parte del ricavo della vendita da 200.000,01 a 350.000 Euro,

un altro 0,5 per cento della parte del ricavo della vendita da 350.000,01 a 500.000 euro e

un altro 0,25 per cento della parte del ricavo della vendita superiore a 500.000 euro.

L’importo complessivo della compensazione del diritto di seguito derivante da una rivendita è pari al massimo a 12.500 euro.

Calcolo commissione particolare sul margine del profitto:

- Prezzo d’aggiudicazione fino a 800.000 euro: provvigione del 32%.

- Per la parte del prezzo d’aggiudicazione superiore a 800.000 euro si calcola una provvigione del 27%, che viene aggiunta a quella relativa alla parte del prezzo d’aggiudicazione fino a 800.000 euro.

- Per la parte del prezzo d’aggiudicazione superiore a 4.000.000 euro si calcola una provvigione del 22%, che viene aggiunta a quella relativa alla parte del prezzo d’aggiudicazione fino a 4.000.000 euro.

Il prezzo d’acquisto comprende l’imposta sul valore aggiunto in vigore in quel momento, attualmente il 19%.

Calcolo regime fiscale normale:

Prezzo di aggiudicazione fino a 800.000 €: supplemento del 27%, più l´IVA legale

Prezzo di aggiudicazione superiore a 800.000 €: Parte del prezzo fino a 800.000 € supplemento del 27 %, parte del prezzo che supera i 800.000 € supplemento del 21%, a talvolta maggiorato dell'IVA legale.

Prezzo di aggiudicazione superiore a 4.000.000 €: Parte del prezzo che supera i 4.000.000 € supplemento del 15%, a talvolta maggiorato dell'IVA legale.

La preghiamo di avvisarci prima della fatturazione nel caso in cui desidera applicare il regime fiscale normale.

Calcolo diritti di seguito:

Per le opere originali di arti figurative e fotografie di artisti viventi o deceduti da meno di 70 anni soggette al diritto di seguito, in tutti i casi suddetti viene riscossa in aggiunta, a liquidazione della compensazione del diritto di seguito dovuto dalla casa d'aste ai sensi del § 26 della legge tedesca sul diritto d'autore (Urheberrechtsgesetz, UrhG), una compensazione del diritto di seguito con le percentuali indicate nel § 26 2° comma UrhG, che attualmente sono le seguenti:

4 per cento della parte del ricavo della vendita da 400,00 euro a 50.000 euro,

un altro 3 per cento della parte del ricavo della vendita da 50.000,01 a 200.000 Euro,

un altro 1 per cento della parte del ricavo della vendita da 200.000,01 a 350.000 Euro,

un altro 0,5 per cento della parte del ricavo della vendita da 350.000,01 a 500.000 euro e

un altro 0,25 per cento della parte del ricavo della vendita superiore a 500.000 euro.

L’importo complessivo della compensazione del diritto di seguito derivante da una rivendita è pari al massimo a 12.500 euro.